Historically high inflation

After three decades of low and stable inflation, the Norwegian and global economy was marked by high inflation in 2022.

The year 2022 reminded us once again that unexpected events can abruptly change the economic outlook. In the aftermath of Russia’s invasion of Ukraine, inflation rose to the highest levels seen since the 1980s, in both Norway and surrounding countries. Price stability is crucial for maintaining a well-functioning economy. When high inflation erodes purchasing power, those with low incomes and the smallest margins are normally impacted hardest. With the aim of curbing inflation, we have raised the policy rate faster than we had envisaged at the beginning of the year. At the same time, we have sought to avoid dampening the economy beyond that required to tackle inflation.

Geopolitical tensions have given rise to new challenges and have changed the threat landscape. Norges Bank has been concerned with, among other things, being equipped to respond effectively to cyber incidents that could threaten financial stability. Uncertainty and high inflation have also had an impact on global financial markets and on the management of the Government Pension Fund Global (the fund). The decline in both equity and bond markets resulted in a sharply negative return on the fund. At the same time, high oil and gas prices have resulted in historically large capital transfers to the fund, which helped sustain its market value.

A changing world poses challenges for both central banking and investment management at Norges Bank. In 2022, we presented Norges Bank’s strategy for the coming years, Strategy 25. The strategy is designed to ensure that we are best able to accomplish our mission and shows our key priorities for the next three years.

In 2022, I took over as Governor and Pål Longva was appointed Deputy Governor. This Annual Report is testimony to what has been a demanding year, but also a very eventful one. I am deeply impressed by the work carried out by my colleagues at Norges Bank in 2022, and how they have dealt with an array of new challenges. In a turbulent world, it is important that we continue to challenge our thought processes and develop the skills of our employees. This is the best way we can accomplish our mission.

Oslo, 8 February 2023

Ida Wolden Bache

Governor

Introduction to Norges Bank

Norges Bank is Norway’s central bank and is responsible for monetary policy and for promoting financial stability and an efficient and secure payment system. Norges Bank also manages the Government Pension Fund Global and Norway’s foreign exchange reserves.

About Norges Bank

The foundation of Norges Bank in 1816 was an important part of the nation-building process following the dissolution of the union with Denmark. The Storting (Norwegian parliament) gave the central bank two main tasks: to issue a Norwegian currency, the speciedaler, and to extend credit to firms and private individuals.

Today, Norges Bank no longer extends credit directly to the public. On the other hand, the Bank has been assigned a number of other tasks that it performs on behalf of the Norwegian people. The Bank has executive and advisory responsibilities in the area of monetary policy, manages Norway’s foreign exchange reserves and the Government Pension Fund Global and is responsible for promoting robust payment systems and financial markets. In addition, the Bank has the sole right to issue Norwegian banknotes and coins.

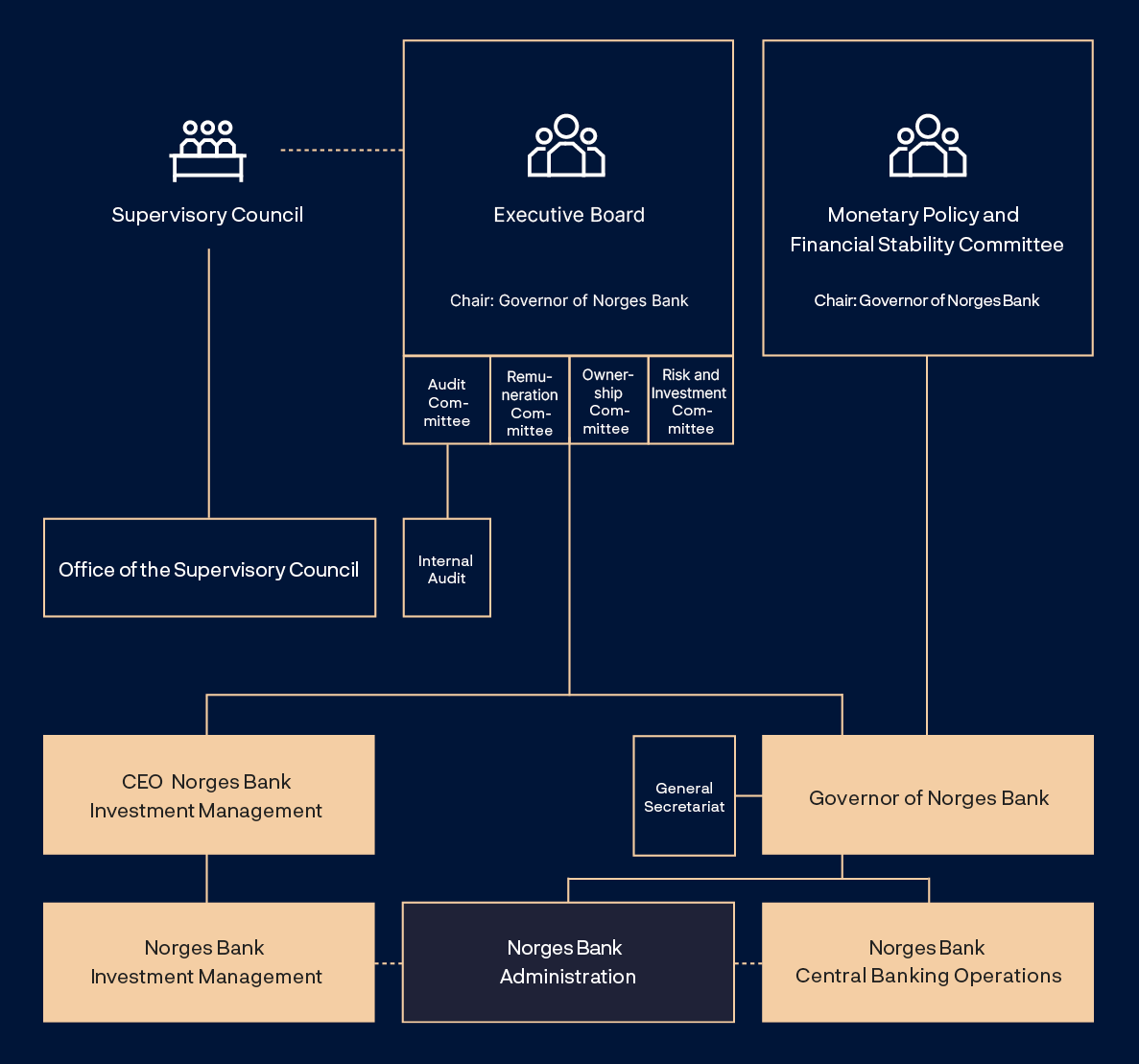

Governance

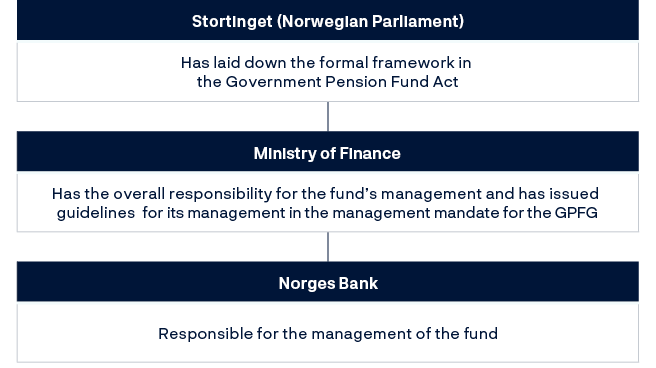

Norges Bank’s activities are regulated by the Act of 21 June 2019 No 31 relating to Norges Bank and the Monetary System etc (the Central Bank Act). Norges Bank’s responsibility for the management of the Government Pension Fund Global is regulated by the Central Bank Act, the Government Pension Fund Act and the management mandate for the fund issued by the Ministry of Finance.

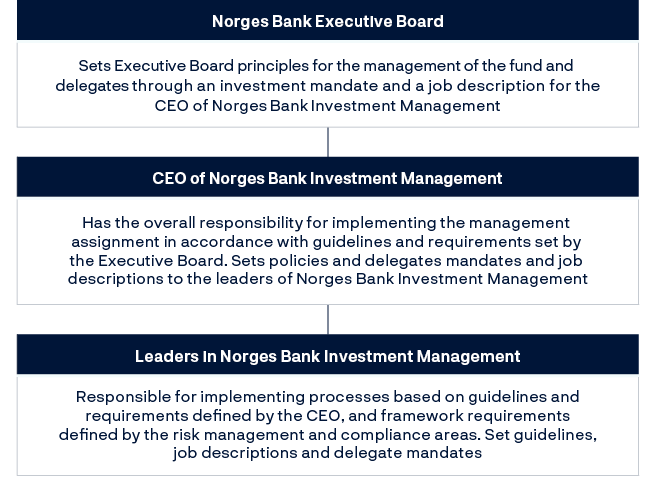

Under the Central Bank Act, the Governor is the general manager of Norges Bank. However, the Executive Board appoints a separate CEO responsible for the management of the Government Pension Fund Global. The Executive Board, which consists of the Governor (Chair), Deputy Governors, and six external members, and two employee representatives who attend Board meetings when administrative matters are on the agenda, is further responsible for ensuring the sound and efficient organisation of the Bank’s operations. The Executive Board is also responsible for the management of the Government Pension Fund Global. The Governor, the two Deputy Governors and the external members are appointed by the King in Council.

The Monetary Policy and Financial Stability Committee comprises the Governor (chair), the two Deputy Governors and two external members. The external members are appointed by the King in the Council of State. The Committee is Norges Bank’s executive and advisory authority for monetary policy and is responsible for the use of instruments to achieve monetary policy objectives. Its aim is to contribute to promoting financial stability by providing advice and using the instruments at its disposal.

Norges Bank’s Supervisory Council is appointed by the Storting and comprises 15 members. The Supervisory Council is Norges Bank’s supervisory body. The Council’s area of responsibility includes approving the budget proposed by the Executive Board, adopting the annual accounts and selecting the Bank’s auditor, and approving the auditor’s plans and expenses.

Organisation

Norges Bank’s governing bodies are the Executive Board, the Monetary Policy and Financial Stability Committee and the Supervisory Council. Norges Bank consists of Central Banking Operations and Norges Bank Investment Management, as well as Norges Bank Administration, a unit that provides shared support functions.

Norges Bank Central Banking Operations is headed by the Governor of Norges Bank and comprises four departments: Monetary Policy, Financial Stability, Markets and IT. The head of Norges Bank Administration also reports to the Governor.

Norges Bank Investment Management is responsible for managing the Government Pension Fund Global. The separate CEO is appointed by the Executive Board. Norges Bank Investment Management comprises the following units: Technology and Operations, Governance and Compliance, Asset Strategies, Equity Strategies, Real Assets, Investment Risk and Staff.

Norges Bank Investment Management is an international organisation with offices in Oslo, London, New York, Shanghai and Singapore, and subsidiaries in Tokyo, Paris and Luxembourg.

Risk management and control

Pursuant to the regulation on risk management and internal control at Norges Bank, regular reviews are conducted of significant risks for all areas of activity.

The Executive Board has the primary responsibility for risk management and for the sound organisation of Norges Bank. Internal Audit supports the Executive Board in its exercise of this responsibility and submits an annual independent assessment of risk management and internal control to the Executive Board.

The division of roles and responsibilities within Norges Bank’s risk management system is organised along “three lines of defence”:

First line of defence: Operational risk management and control activities. Risk assessment and compliance are required to be an integral part of the Bank’s business processes and include the management of outsourced services.

Second line of defence: The key risk management and compliance functions advise and support the departments. Their responsibility is to challenge the assessments made by the first line of defence and monitor the first line of defence to ensure that appropriate controls are carried out. The second lines of defence in the Norges Bank Central Banking Operations and Norges Bank Investment Management report to the Governor of Norges Bank and the CEO of Norges Bank Investment Management, respectively.

Third line of defence: Internal Audit reports to the Executive Board and is required to assess, independently of the administration, whether risk management and compliance function as intended.

The Supervisory Council has primary responsibility for supervising the Bank’s operation and compliance with formal frameworks. The Supervisory Council selects the Bank’s external auditor and submits an annual report to the Storting.

Norges Bank’s Executive Board

The Executive Board comprises the Governor, the two Deputy Governors and six external board members, all appointed by the King in the Council of State. In addition, two board members are selected by and among employees to participate when administrative matters are on the agenda.

The Governor is chair, and the two Deputy Governors are first deputy chair and second deputy chair of the Executive Board. The Executive Board has four preparatory and advisory committees, whose work is to strengthen and streamline the Executive Board’s discussions.

Audit Committee

The Committee’s tasks, in accordance with instructions relating to risk management and internal control at Norges Bank, focus on the monitoring, supervision and control of Norges Bank’s financial reporting, operational risk, compliance, and risk management and internal control systems.

The Audit Committee has three members elected by and from among the external members of Norges Bank’s Executive Board. Internal Audit is to provide the Committee with necessary assistance.

Remuneration Committee

The Remuneration Committee contributes to thorough and independent discussions of matters pertaining to Norges Bank’s salary and remuneration schemes. The Executive Board has decided that the statutory Remuneration Committee for Asset Management is to also prepare matters relating to Norges Bank Central Banking Operations.

The Committee comprises three members elected from among the external members of Norges Bank’s Executive Board and one member elected from among the employee-elected board members.

Ownership Committee

The Ownership Committee is a preparatory body for the Executive Board on matters related to Norges Bank’s responsible investment activities. The Committee prepares matters related, for example, to the observation or exclusion of companies from the investment universe of the Government Pension Fund Global, within the framework laid down in the Ministry of Finance’s management mandate and the ethical guidelines for the management of the Government Pension Fund Global.

The Ownership Committee comprises three members and is chaired by the Deputy Governor of Norges Bank with particular responsibility for following up management of the Government Pension Fund Global. The other two members are elected among the Executive Board’s external members.

Risk and Investment Committee

The Risk and Investment Committee strengthens and streamlines the Executive Board’s work related to investment strategy, current exposure, performance assessment, determination and use of risk limits, and major investment decisions.

The Risk and Investment Committee comprises three members and is chaired by the Deputy Governor of Norges Bank with particular responsibility for following up the management of the Government Pension Fund Global. The other two members are elected among the Executive Board’s external members.

Work of the Executive Board in 2022

The Executive Board held 14 meetings and discussed 212 items of business in 2022. Meetings also take place in the form of seminars for more in-depth presentations and discussions with the administration on the premises for important items on the Board’s agenda.

In addition, time is spent by the Executive Board’s four subcommittees on preparing selected matters to be considered by the Executive Board.

The Executive Board’s time for the period 2018-2019 was relatively evenly distributed between central banking operations and investment management. In the period 2020 and 2022, approximately two thirds of the Board’s time was spent on investment management. This is a consequence of the new Central Bank Act where the newly established Monetary Policy and Financial Stability Committee had been assigned responsibility for areas that were previously the responsibility of the Executive Board.

Table 1 Work of the Executive Board 2018–2022.

|

2018 |

2019 |

2020 |

2021 |

2022 |

|

|

Number of Executive Board meetings |

18 |

18 |

20 |

14 |

14 |

|

Number of Executive Board seminars |

10 |

11 |

4 |

5 |

6 |

|

Number of matters considered by the Executive Board |

232 |

242 |

222 |

228 |

212 |

|

Committee meetings |

|||||

|

Audit Committee |

7 |

5 |

7 |

11 |

7 |

|

Remuneration Committee |

6 |

4 |

5 |

7 |

4 |

|

Ownership Committee |

5 |

5 |

7 |

9 |

7 |

|

Risk and Investment Committee |

6 |

7 |

10 |

13 |

13 |

Members of the Executive Board

Ida Wolden Bache

Appointed Governor of Norges Bank from 8 April 2022 to 2028. Bache is Chair of the Executive Board and the Monetary Policy and Financial Stability Committee.

Her work experience includes posts as Deputy Governor, Executive Director of Norges Bank Monetary Policy and Norges Bank Financial Stability. She has also been a macroeconomist at Handelsbanken Capital Markets. Bache was a member of the Systemic Risk Council in Denmark in the period between 2017 and 2022. She holds a doctorate in economics from the University of Oslo and an MSc in economics from the London School of Economics.

Pål Longva

Appointed Deputy Governor for the period 29 August 2022 through 2028. Longva has particular responsibility for central banking operations and is First Deputy Chair of the Executive Board and the Monetary Policy and Financial Stability Committee.

His work experience includes the post of Director General of the Ministry of Finance Budget Department. Longva has worked at McKinsey and as Deputy Director General and Director General at the Ministry of Labour and Social Inclusion. He holds a doctorate in economics from the University of Oslo.

Øystein Børsum

Appointed Deputy Governor for the period 2 August 2021-2027. Børsum has particular responsibility for the Government Pension Fund Global. Børsum is Second Deputy Chair of the Executive Board and the Monetary Policy and Financial Stability Committee.

His work experience includes the post of chief economist at Swedbank and positions in the Budget and Asset Management Departments of the Ministry of Finance. Børsum holds a degree in economics from the NHH Norwegian School of Economics, masters’ degrees from Sciences Po and London School of Economics and a doctorate in economics from the University of Oslo.

Karen Helene Ulltveit-Moe

Appointed board member for the period to 15 May 2024. Chair of the Audit Committee and member of the Remuneration Committee of the Executive Board.

Ulltveit-Moe holds a professorship in the Department of Economics of the University of Oslo. She is chair of the NHH Norwegian School of Economics board and has held a number of directorships. She also chaired and was a member of several government-appointed commissions. Her main research interests are in international economics, tax policy and industrial policy. She is Research Fellow at the Centre for Economic Policy Research (CEPR) and CESifo and is an elected member of the Norwegian Academy of Science and Letters. Ulltveit-Moe holds an MSc in economics from the University of Mannheim and a PhD in economics from the NHH Norwegian School of Economics.

Kristine Ryssdal

Appointed board member for the period to 15 May 2026. Member of the Ownership Committee and the Remuneration Committee of the Executive Board.

Ryssdal is General Counsel at Yara. Other previous professional experience includes the positions of VP Legal at Statoil, (now Equinor), Chief Legal Officer at REC and Legal Counsel at Norsk Hydro. She served for several years as an attorney at the Office of the Attorney General. She has previously been a member of the board at Borregaard ASA, previously held various board positions in the REC group and was a member of Kommunalbanken Norway’s Supervisory Board. Ryssdal holds a degree in law (Cand. jur.) from the University of Oslo and a Master of Laws from the London School of Economics. She is also qualified to appear before the Supreme Court.

Arne Hyttnes

Appointed board member for the period to 15 May 2026. Chair of the Remuneration Committee and member of the Audit Committee of the Executive Board.

Hyttnes has extensive experience from the financial industry, including positions at DnC/DnB, the Norwegian Savings Banks Association, Finance Norway and the Norwegian Banks’ Guarantee Fund. He was managing director of the Norwegian Industrial and Regional Development Fund for four years and also has board experience from the NHH Norwegian School of Economics and “Ungt Entreprenørskap”, a non-profit organisation to promote cooperation between schools and the business sector. Hyttnes holds a degree in economics and business administration from the NHH Norwegian School of Economics.

Hans Aasnæs

Appointed board member for the period to 15 May 2024. Member of the Risk and Investment Committee of the Executive Board.

Aasnes is CEO of the shipping company Western Bulk ASA. He is chair of the board at Strand Havfiske, Nordic Trustee and Investinor. He has extensive experience in investment management, real estate management and direct investment at Storebrand and the UMOE Group, among others. He also has extensive board experience from a number of companies, including the Government Pension Fund Norway, Statskog, Gjensidige pensjonsforsikring, Bergvik Skog, Foran Realestate and Fornebu Lumber Company. Aasnes is an agricultural economist from the Norwegian College of Agriculture (now the Norwegian University of Life Sciences), holds a higher degree from the NHH Norwegian School of Economics and is a certified financial analyst.

Nina Udnes Tronstad

Appointed board member for the period to 15 May 2026. Member of the Audit Committee and the Ownership Committee of the Executive Board.

Udnes Tronstad is a professional board member. She is chair of the board at Source Energy and a member of the board at Bladt Industries and Prosafe. She was executive vice president at Kværner and Statoil (now Equinor). She has been a board member at Peab AB, Trelleborg AB, Rambøll, Giek (now Eksfin) and the Norwegian University of Science and Technology (NTNU) among others. Udnes Tronstad holds an MSc in chemical engineering from the Norwegian University of Science and Technology.

Egil Herman Sjursen

Appointed board member for the period to 15 May 2024. Member of the Risk and Investment Committee of the Executive Board.

Sjursen stepped down as Chief Executive Officer of Holberg Fondsforvaltning in 2018 after having served in this position for 12 years. He has held executive positions in asset management in DNB (including London), Vesta Forsikring and Nordea Investment Management since the end of the 1980s. Egil Herman Sjursen is currently chair of the board at the Bergen Philharmonic Orchestra, Stiftelsen Universitetsforskning i Bergen (Unifob), Nysnø Klimainvesteringer AS and the Nibor Oversight Committee. Sjursen has held a number of board positions. Sjursen holds a postgaduate degree in social sciences (cand. polit.), with a major in economics, from the University of Bergen.

Employee-elected board members

Mona Sørensen

Employee representative from 1 January 2016.

Member of the Remuneration Committee of the Executive Board.

Chair and chief union representative of the Finance Sector Union of Norway at Norges Bank. Mona Sørensen holds a degree in economics and administration and an Executive Master of Management with a specialisation in applied organisational psychology from the BI Norwegian Business School.

Marianne Depraetere is alternate for Mona Sørensen.

Truls Oppedal

Employee representative from 1 January 2021.

Deputy chair of the Federation of Norwegian Professional Associations. Truls Oppedal holds a master’s degree in Business and Finance from Heriot-Watt University in Edinburgh, Scotland.

Kjersti Gro Lindquist is alternate for Truls Oppedal.

Annual Report of the Executive Board for 2022

2022 was another challenging year for Norges Bank. The pandemic and the war affected all of Norges Bank’s activities and the work of the employees.

The beginning of 2022 was affected by the Covid-19 pandemic. Norges Bank’s premises at Bankplassen were closed down and most employees worked remotely. When the government announced that Norway could reopen on 12 February, the Bank allowed employees to return to the office.

On 24 February, only a few days after society reopened, Russia invaded Ukraine. The impact of the war and the after-effects of the pandemic influenced Norges Bank’s work throughout 2022. The employees put in considerable effort in a demanding period. The Executive Board is satisfied that high performance and professional standards have been maintained and wish to express their thanks to Norges Bank’s employees. 2022 saw substantial movements in global financial markets. Russia’s invasion of Ukraine contributed to a sharp rise in energy prices in Europe. Together with strong demand and supply-side constraints, this led to a marked rise in global inflation. The Monetary Policy and Financial Stability Committee has therefore raised the policy rate more and faster than projected at the beginning of 2022. See the Committee’s Report for more information.

The return on the Government Pension Fund Global closely follows developments in global equity and bond markets. In 2022, interest rates rose, and both equity and bond market returns were negative. Weak markets during the year resulted in an overall return on the fund of -14.1%. The market value of the fund at year-end 2022 was NOK 12 429bn.

In 2022, Norges Bank worked to develop the payment system in a number of areas. The Bank has entered into formal discussions with the European Central Bank (ECB) on possible participation in the Eurosystem’s TARGET Instant Payment Settlement (TIPS) service. The research into central bank digital currencies (CBDCs) has continued, and Norges Bank and Finanstilsynet (Financial Supervisory Authority of Norway) are working together to test cyber resilience in accordance with the TIBER (threat intelligence-based ethical red teaming) framework in Norway.

2022 was the last year of the strategy period 2020-2022. In the assessment of the Executive Board, Norges Bank largely achieved the ambitions in the strategy, despite the dramatic changes caused by the pandemic and the war in Ukraine. The strategy for the next three years, Strategy 25, was approved by the Executive Board in November 2022. This comprises an overarching strategy for Norges Bank as a single institution and one strategy for each of the operational areas: the central bank and Norges Bank Investment Management. See Section 4 for more details on the strategy.

In 2022, a number of changes were made to Norges Bank’s executive management. In 2021, Governor Øystein Olsen announced his intention to step down on 1 March 2022. Deputy Governor Ida Wolden Bache temporarily occupied the post of Governor from 1 March 2022 and was appointed Governor from 8 April 2022. On 29 August, Pål Longva assumed the post of Deputy Governor, succeeding Ida Wolden Bache.

Management of the Government Pension Fund Global

Norges Bank manages the Government Pension Fund Global on behalf of the Ministry of Finance. Norges Bank’s mandate is to achieve the highest possible long-term return with an acceptable level of risk and within the constraints laid down in the mandate from the Ministry of Finance.

The management of the fund in 2022

The market value of the Government Pension Fund Global at year-end 2022 was NOK 12 429bn. The fund’s market value is affected by the return on investments, capital inflows and withdrawals by the government and exchange rate movements.

The return in 2022 was equivalent to NOK -1 637bn. Movements in the krone exchange rate increased the market value by NOK 642bn, but this has no bearing on the fund’s international purchasing power. Inflow of capital from the Norwegian government came to NOK 1 085bn net after the payment of management fees. This is the largest annual inflow since the fund was formed. The new capital was phased into the fund in an effective way.

At year-end 2022, asset allocation was 69.8% equities, 27.5% fixed income, 2.7% unlisted real estate and 0.1% unlisted renewable energy infrastructure.

In 2022, the return on the Government Pension Fund Global before management costs was -14.1% in terms of the fund’s currency basket. Equities returned -15.4%, bonds -12.1%, unlisted real estate 0.1% and unlisted renewable energy infrastructure 5.1%. Management costs amounted to 0.04% of assets under management.

Norges Bank manages the fund close to the benchmark index, but all investment processes have active components. This puts Norges Bank in a better position to generate the highest possible return and be a responsible investor. Norges Bank uses a range of investment strategies in its management of the fund. They are grouped into three main categories: market exposure, security selection and fund allocation. Norges Bank has reported contributions to the relative return from the same three strategies throughout the period since 2013. Management within each category has, however, been subject to change.

The bulk of the Government Pension Fund Global is managed under the strategy for market exposure. The main aim of this strategy is to achieve market exposure mirroring the benchmark index as cost-efficiently as possible. Transaction costs are minimised by avoiding mechanical replication of index changes. An excess return is also generated by pursuing various indexing strategies.

Security selection is based on fundamental analysis, and Norges Bank uses both internal and external mandates. Specialist expertise and delegated mandates allow investment decisions to be made independently of the market consensus.

Fund allocation is the strategy that made the largest positive contribution to the excess return in 2022. This strategy exploits how a long investment horizon and a limited need for liquidity make it possible to accept substantial fluctuations in the fund’s value and to invest even where it may take a long time to realise the underlying value. Investments in unlisted real estate and unlisted renewable energy infrastructure are part of the allocation strategy. Norges Bank can also act differently to other funds in challenging market situations. At the beginning of the year, the fund had a slightly smaller allocation to equities than the benchmark index, and its bond investments had a lower duration. This helped the fund to outperform the benchmark in 2022.

Norges Bank applies these different strategies across the fund’s various asset classes. The contributions to the relative return from equity, fixed income and real asset management show that management of fixed income contributed the most to excess return in 2022.

In 2022, Norges Bank achieved an overall return before management costs that was 0.87 percentage point higher than the return on the fund’s benchmark index. The Executive Board notes that all three main strategies contributed positively to this excess return.

Performance measured over time

The Executive Board emphasises the importance of assessing performance over time, and is satisfied that the return, both in 2022 and over time, has been higher than the return on the benchmark index the fund is measured against.

In the period between 1998 and 2022, the annual return on the fund was 5.7%. The annual net real return, after deductions for inflation and management costs, was 3.5%.

Over the same period, the annual return before management costs was 0.30 percentage point higher than the return on the benchmark index from the Ministry of Finance. In the period since 2013, during which the strategies have been grouped into market exposure, security selection and fund allocation, the annual excess return before management costs has been 0.33 percentage point. The contributions from the three main strategies show that fund allocation has made a slightly negative contribution to the relative return, while market exposure and security selection have both made a positive contribution.

The objective of the highest possible return is to be achieved with acceptable risk. Risk is measured, analysed and followed up using a broad set of measures and analyses. The management mandate requires Norges Bank to manage the fund with a view to ensuring that expected relative volatility (tracking error) does not exceed 1.25 percentage points. Expected relative volatility was 0.39 percentage point at the end of 2022, compared with 0.50 percentage point a year earlier.

Measured over the full period since 1998, realised relative volatility has been 0.65 percentage point.

The management of the fund is to be cost-effective. Cost-effective management supports the objective of the highest possible return after costs. In the period between 2013 and 2022, annual management costs averaged 0.05% of assets under management. In 2022, management costs amounted to NOK 5.2bn, or 0.04% of assets under management. The Executive Board is satisfied that management costs are low compared to other managers.

Further development of the investment management

Norges Bank’s Executive Board adopted a new strategy plan for the management of the Government Pension Fund Global at the end of 2022. The plan builds on previous strategy plans but makes minor adjustments to the three main strategies. These strategies are complementary and seek to exploit the fund’s size and long investment horizon.

The mandate from the Ministry of Finance requires responsible investment to be an integral part of the management of the fund. A good long-term return is considered to depend on sustainable economic, environmental and social development. The management of climate risk is a priority for Norges Bank’s work on responsible investment. The Ministry added a specific climate target for this work to the mandate for Norges Bank in 2022, along with new requirements for measuring, managing and reporting on climate risk. The Executive Board is pleased that Norges Bank has published a clear climate action plan for the period 2022–2025.

The work to integrate responsible investment into the management of the fund is described in the section Sustainability work in Norges Bank.

See the Annual report 2022, Government Pension Fund Global for more information on the management of the fund.

Management of the foreign exchange reserves

The foreign exchange reserves are held for the purpose of crisis management and are to be used as part of the conduct of monetary policy, to promote financial stability and to meet Norges Bank’s international commitments. Considerable weight is given to the importance of investing the reserves in liquid assets. The aim of the management of the foreign exchange reserves is to attain the highest possible return within the set management limits.

Management of the reserves in 2022

The market value of the foreign exchange reserves was NOK 610.0bn at year-end 2022, which is NOK 32.6bn less than in 2021. The foreign exchange reserves are divided into an equity portfolio, a fixed income portfolio and the petroleum buffer portfolio. The value of the equity portfolio was NOK 110.4bn, the value of the fixed income portfolio was NOK 472.0bn and the value of the petroleum buffer portfolio was NOK 27.6bn.

Return in international currency terms reduced the value of the reserves by NOK 53.1bn in 2022. Contributions from the equity and fixed income portfolios were NOK -15.9bn and NOK -38.7bn, respectively. A weaker krone increased the value of the reserves by NOK 44.3bn. Net outflows were NOK 25.6bn, primarily from the petroleum buffer portfolio.

In 2022, the return on the equity portfolio and the fixed income portfolio was -9.4% in international currency terms. Equity investments returned -16.8%, while fixed income investments returned -7.5%. In NOK terms, the total return was NOK -2.5%. The results reflect lower share prices and higher global higher interest rates. A weaker krone dampened the impact in NOK terms.

The foreign exchange reserves are managed close to benchmark indexes set by the Executive Board, and the return closely tracks global equity and bond market developments. In 2022, the return on the equity and fixed income portfolios was 0.1 percentage point and 0.07 percentage point higher than the return on the portfolios’ benchmark indexes, respectively. The Executive Board is satisfied with the return, which was higher than in the benchmark indexes in a year of negative returns.

Extraordinarily high oil and gas prices through 2022 entailed extra capital flows and large swings in the petroleum buffer portfolio through the year. The purpose of the portfolio is to provide for appropriate management of the government’s need for converting foreign currency and NOK, and for any transfers to and from the Government Pension Fund Global. The portfolio normally fluctuates in value owing to the purchase or sale of currency in the market, the purchase of foreign exchange from the State’s Direct Financial Interest in petroleum activities (SDFI), and monthly transfers to and from the Government Pension Fund Global. In total, agreements were entered into for more than NOK 26 000bn in the foreign exchange reserves.

The integration of responsible investment into the management of the foreign exchange reserves is discussed in the section . See the report Management of Norges Bank’s foreign exchange reserves for more information on the management of the Bank’s foreign exchange reserves.

Government debt management

Norges Bank provides services in connection with government borrowing on behalf of the Ministry of Finance.

The government’s borrowing requirement is primarily met through long-term borrowing in the market (government bonds) at a fixed interest rate. The government also borrows short-term by selling Treasury bills, which are debt instruments with a maturity of one year or less. The government borrows exclusively in NOK.

The management in 2022

At year-end 2022, government debt totalled NOK 596bn, with NOK 532bn in government bonds and NOK 64bn in Treasury bills. Of this amount, the government’s own stock amounted to NOK 66bn in bonds and NOK 24bn in Treasury bills.

NOK 20bn was borrowed through a new 10-year bond issued in February by syndication. In September, a new 20-year bond worth NOK 10bn was issued by syndication. This was the first time a Norwegian government bond was issued with maturity longer than 11 years. Existing bonds were reopened in the amount of NOK 34bn at 17 auctions. NOK 12bn was issued to the government’s own stock in the course of 2022.

Treasury bills worth NOK 57.65bn were issued to the market at 18 auctions. NOK 24bn was also issued to the government’s own stock in the course of 2022.

In 2022, the average auction premium, measured as the difference against the mid-yield in the market, at bond issuance was -0.002 percentage point compared with 0.022 percentage point in 2021. At the end of June, owing to high volatility and uncertainty in foreign and domestic government securities markets, Norges Bank allowed primary dealers to quote higher yield spreads than normal in the interdealer market for bonds and bills. This exception was retained a number of times and remained in effect at the end of 2022.

The average yield for bonds issued in 2022 was 2.76%, compared with 1.24% in 2021. The increase reflected a general rise in interest rates.

The Executive Board is satisfied with the management of government debt in 2022.

Payment system

Norges Bank is tasked with promoting an efficient, secure and attractive payment system. Norges Bank is the ultimate settlement system for interbank payments in Norway and also issues banknotes and coins. Norges Bank oversees the payment system and other financial infrastructure, contributes to contingency arrangements and is the supervisory authority for interbank systems. The operation of the financial infrastructure in Norway was stable in 2022.

Norges Bank’s settlement system

Payment settlement between banks and other financial sector undertakings with an account at Norges Bank takes place in Norges Bank’s settlement system (NBO). Thus, most payments in NOK are ultimately settled in NBO. The operation of NBO was stable through 2022. In 2022, NBO handled a daily average of approximately NOK 339bn in payment transactions. At year-end 2022, banks’ sight deposits and reserves on deposit with Norges Bank totalled NOK 26.3bn.

A well-functioning solution for real-time payments is an important part of an efficient payment system. Norges Bank has entered into formal discussions with the European Central Bank on possible participation in the Eurosystem’s TARGET Instant Payment Settlement (TIPS) service. The primary objective is to facilitate the development of real-time payment services by banks and other market participants in the Norwegian payment system. Norges Bank is in the process of reviewing and assessing the TIPS service at a detailed level, including the technical setup, security, contingency arrangements and costs. This work will lead to a basis for deciding on possible participation in TIPS, which safeguards Norges Bank’s requirements and the needs of other relevant stakeholders. In connection with Strategy 25, the Executive Board has decided to begin the process of overhauling the settlement system.

Cash

The public’s access to central bank money in the form of cash is a key feature of the payment system. Cash usage in Norway has declined over many years, and the decline accelerated during the pandemic. Twice a year, Norges Bank conducts surveys on households’ use of cash. The autumn 2022 survey showed that 4% of payments in shops and 4% of payments between private individuals (person-to-person) were made in cash, ie unchanged since spring 2022.

Many of the attributes of cash are of such a nature that they will continue to be important even in the event of falling cash usage. In addition to being central bank money, the fact that cash can be used independent of third parties or electronic systems is crucial for financial inclusion and contingency arrangements. In Norges Bank’s opinion, it is important to ensure that cash remains available and easy to use so that it can fulfil its functions in the payment system.

Central bank digital currency

The structural changes in the payment system raise questions about whether there is a need for Norges Bank to implement measures to ensure that payments can continue to be made efficiently and securely in NOK in the future. One key question is whether Norges Bank should provide central bank money to the public in digital as well as physical form, termed central bank digital currency (CBDC). Norges Bank is in the process of exploring this issue, motivated by both declining cash usage and a desire to be prepared to introduce a CBDC if necessary for the Norwegian payment system to develop in a desirable manner.

Norges Bank’s research into CBDC is now in its fourth phase. Up until summer 2023, the Bank will carry out experimental testing of different technical CBDC solutions and continue its work on analysing the purpose and consequences of a potential introduction of a CBDC. As part of Strategy 25, the Executive Board has approved that Norges Bank, during the strategy period, will prepare the ground for the issue, if appropriate, of a CBDC.

Cyber resilience of the financial system

Cyber incidents are a potential threat to the financial system and financial stability. Globally, there is broad agreement that resilience against cyber attacks in the financial sector must be strengthened. This requires extensive public-private cooperation. Norges Bank and Finanstilsynet are working together to introduce cyber resilience testing in accordance with the TIBER framework in Norway (TIBER-NO) to bolster the cyber resilience of the financial system. Entities with responsibility for critical functions in the banking and payment system have agreed to be part of the TIBER-NO Forum. The first tests started in autumn 2022.

See Financial Infrastructure Report 2022 for more information on the payment system.

Staff

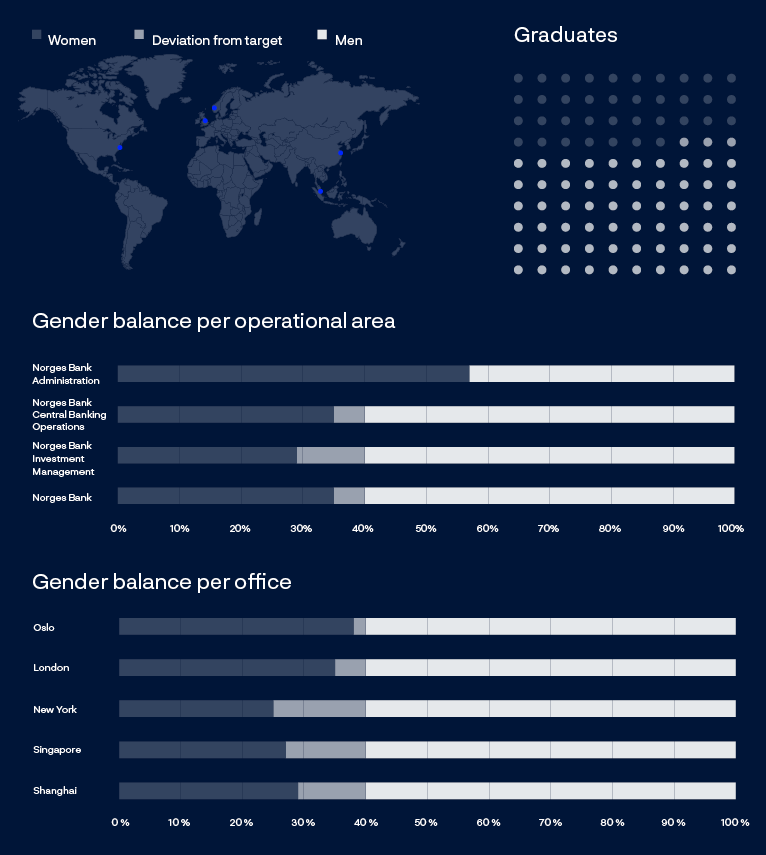

At year-end 2022, Norges Bank had 1007 permanent employees. Of these, 572 were in Norges Bank Investment Management, 272 in Norges Bank Central Banking Operations and 156 in Norges Bank Administration. In addition, seven employees worked at the Office of the Supervisory Council. Norges Bank has employees from 39 countries and offices in Oslo, London, New York, Shanghai and Singapore. Norges Bank also has subsidiaries in London, Paris, Luxembourg and Tokyo.

Competent staff are important to the fulfilment of Norges Bank’s mission, and they are required to have relevant expertise, insight and a high level of integrity.

Norges Bank works systematically to attract and recruit top candidates from leading national and international academic institutions. Norges Bank works continuously with career development, for example by offering targeted courses and study programmes.

Norges Bank aims to achieve gender balance and diversity in the workforce. The objective is a gender balance of at least 40% as a whole and the ambition is to increase the number of women in management positions and in specialist functions. Norges Bank is also one of the founding partners of Norway’s Women in Finance Charter.

The share of women on the permanent staff of Norges Bank at year-end 2022 was 35%, compared with 34% in 2021. The share of women in the different areas was 29% in Norges Bank Investment Management, 35% in Norges Bank Central Banking Operations and 57% in Norges Bank Administration.

The Executive Board is not satisfied with the overall gender balance and will closely follow up the initiatives for achieving the target.

The relationship between Norges Bank’s management, staff and the Bank’s trade union representatives must be based on dialogue, confidence and mutual respect. The management has close contact with the representatives at Norges Bank, for example in the Co-determination and Personnel Committee, the Working Environment Committee and regular contact meetings with representatives at several levels in Norges Bank.

Norges Bank’s priority is to protect the health and safety of all staff. Nine workplace accidents or injuries directly relating to work conducted at Norges Bank’s premises were reported in 2022, none of which were severe or reported as occupational injuries to the Norwegian Labour Inspection Authority. Sickness absence in 2022 remained stable at a low level of 2.3%.

See the section on Governance, ethics and culture for more information on Norges Bank’s staff.

Corporate governance

Norges Bank’s governance framework aims to be in line with best practice. The Executive Board follows up the operations through periodic reporting on performance and goals, action plans, budgets, financial and operational risk and compliance.

Norges Bank’s use of resources is required to be cost-efficient and prudent, with a cost level that is reasonable compared with that of similar organisations. Benchmarking, ie external comparisons of Norges Bank’s use of resources with that of other similar organisations, is used as a corporate governance tool. During 2022, comparisons were conducted of management costs for the Government Pension Fund Global against 270 other funds. Size and asset composition are considered to achieve the best possible basis for comparison. The Government Pension Fund Global is the fund in the comparison group with the lowest costs measured as a share of assets under management.

Norges Bank complies with the Instructions relating to risk management and internal control at Norges Bank issued by the Ministry of Finance. The Executive Board has issued principles for risk management. In addition, the Ministry of Finance defines limits for the management of the Government Pension Fund Global, including allocation of asset classes and the benchmark index. The Executive Board sets similar limits for the management of the foreign exchange reserves. There were no breaches of the limits for the management of the Government Pension Fund Global or the foreign exchange reserves in 2022. Valuations, performance measurement, management and control of risk in investment management comply with internationally recognised standards and methods. See the notes to the financial statements for more detailed information.

Reporting and following up risks and incidents constitute an important part of the measures to improve operations and internal control. Significant risks are followed up through regular reporting and follow-up of Executive Board measures. The Executive Board has set a 12-month risk tolerance limit for Norges Bank Investment Management specifying that the probability that operational risk factors will result in a gross loss of NOK 750m or more must be less than 20%. In 2022, operational risk exposure was within the Board’s risk tolerance limit.

The Executive Board continuously monitors operational and financial risk through its assessment of operational risk and internal control. The Executive Board submits an annual risk assessment to the Supervisory Council based on reporting by the administration and Internal Audit.

No material deficiencies in the risk management and control regime were identified in 2022, and the Executive Board assesses the control environment and control system at Norges Bank as satisfactory.

No directors’ and officers’ liability insurance has been provided for the members of the Executive Board or the chair of the Board, ie the Governor, in her role as general manager of Norges Bank. In practice, the Board members have limited liability risk, and the Bank therefore self-insures any liability for damages on behalf of Board members or equivalent executive management positions. This is in line with practice in other Nordic central banks.

Security and IT systems

Norges Bank faces a complex threat landscape in constant flux, influenced by geopolitical developments.

The continuous assessment of Norges Bank’s assets, threats and vulnerabilities are important for the ongoing identification and implementation of risk mitigation measures. A range of training activities are also conducted, such as phishing drills and e-learning modules, to strengthen awareness among staff of current security threats. Relevant controls are performed based on frameworks and standards for best practice. Norges Bank uses the US National Institute of Standards and Technology Cyber Security Framework (NIST CSF) for its management of information and IT security risks.

Stable IT systems are essential for Norges Bank to fulfil its mission. The Bank works systematically to ensure a high level of operational stability and has sound disruption management and change management processes in place.

Norges Bank gives weight to automation, innovation, the replacement of outdated IT solutions and robust information security measures. This work is also highlighted in the strategic plan adopted for the following period. An operationally robust organisation helps to secure Norges Bank’s values. Since the completion of the multi-year project to modernise Norges Bank Central Banking Operation’s IT operating platforms, collaboration with new suppliers has been operationalised. The new IT operating platforms have had a high level of accessibility through the year, and no faults have occurred that have affected Norges Bank’s capacity to perform its mission. In the course of 2022, some IT functions, such as the IT helpdesk in Norges Bank Investment Management, were insourced to increase quality and improve flexibility.

Digital threats and organised cyber criminals represent a growing risk as agents are becoming more specialised, sophisticated and well-funded. IT security was strengthened in 2022. The number of employees working in security, particularly cyber resilience, has increased, at the same time as the use of external consultants in this area has been reduced. The employee IT security training programme has been expanded. There were no security incidents with serious consequences in 2022.

Balance sheet and financial statements

Norges Bank’s balance sheet

Norges Bank’s balance sheet contains a number of items directly related to the Bank’s mission. The balance sheet total at year-end 2022 was NOK 13 200bn, compared with NOK 13 172bn at year-end 2021.

In line with the management mandate for the Government Pension Fund Global, the Ministry of Finance has placed a portion of the government’s assets in a separate account in Norges Bank (the GPFG’s krone account), presented as a liability to the Ministry of Finance. Norges Bank reinvests these funds, in its own name, and presents this as net value GPFG. The value of the GPFG’s krone account will always equal the value of the investment portfolio less accrued management fee. Norges Bank, in its role as asset manager, bears no financial risk associated with the management of the Government Pension Fund Global. At year-end 2022, the market value of the fund’s investments was NOK 12 429bn, compared with NOK 12 340bn at year-end 2021. See the separate section Management of the Government Pension Fund Global in the Report for more details on the management of the fund in 2022.

Detailed financial reporting for the investment portfolio of the Government Pension Fund Global is presented in Note 20 to the financial statements. In addition, a separate annual report on the management of the fund has been published.

Excluding the Government Pension Fund Global, the foreign exchange reserves are Norges Bank’s largest balance sheet asset. The foreign exchange reserves are primarily invested in equities, fixed income instruments and cash. Net foreign exchange reserves amounted to NOK 610bn at year-end 2022, compared with NOK 643bn at year-end 2021. See the separate section on Management of the foreign exchange reserves in the Report for more details on the management of the foreign exchange reserves.

Under the government’s consolidated account system, all government liquidity is collected in government accounts at Norges Bank. At year-end 2022, deposits amounted to NOK 305bn, compared with NOK 344bn at year-end 2021. Except for the GPFG krone account, this is the largest liability item on the balance sheet. However, this item fluctuates considerably through the year owing to substantial incoming and outgoing payments over the government’s accounts and transfers to and withdrawals from the Government Pension Fund Global.

Banknotes and coins in circulation are a liability item for Norges Bank. Norges Bank guarantees the value of this money. The amount of cash in circulation is driven by public demand. In recent years, lower demand for cash has reduced the amount in circulation. At year-end 2022, banknotes and coins in circulation amounted to NOK 40bn, unchanged compared with year-end 2021.

Deposits from banks, comprising sight deposits, reserve deposits and F-deposits, are managed by Norges Bank in accordance with its liquidity management policy. At 31 December 2022, these deposits amounted to NOK 27bn, compared with NOK 23bn at year-end 2021.

Norges Bank administers Norway’s financial obligations and rights ensuing from participation in the International Monetary Fund (IMF). Norges Bank has therefore both claims on and liabilities to the IMF. At year-end 2022, Norway’s net position with the IMF amounted to a claim of NOK 23bn, compared with NOK 19bn at year-end 2021. See Note 17 in the notes to the financial statements for more details on the relationship between Norges Bank and the IMF.

Norges Bank’s equity at 31 December 2022 was NOK 270bn, compared with NOK 289bn at 31 December 2021. The Bank’s equity consists of the Adjustment Fund and the Transfer Fund. At year-end 2022, the Adjustment Fund stood at NOK 253.3bn and the Transfer Fund at NOK 16.2bn, compared with NOK 266.5bn and NOK 22.2bn, respectively, at year-end 2021. Norges Bank’s equity, excluding the GPFG’s krone account, was 35% of the balance sheet total, compared with 34.7% in 2021. The Executive Board deems that the Bank’s equity is sufficient to fulfil the Bank’s purpose (cf Section 3-11, Sub-section 1, of the Central Bank Act).

This balance sheet composition is normally expected to generate a positive return over time, excluding foreign currency effects, as returns on the Bank’s investments in equities and fixed income instruments are expected to exceed the cost of the Bank’s liabilities. Norges Bank’s assets are primarily invested in foreign currency, whereas its liabilities are primarily in NOK.

Given the Bank’s balance sheet composition, income will largely be affected by developments in global fixed income, equity and foreign exchange markets. Considerable volatility in income should be expected from year to year. Future increases in the value of the Government Pension Fund Global will be affected by, among other things, transfers to/from the fund.

Income statement

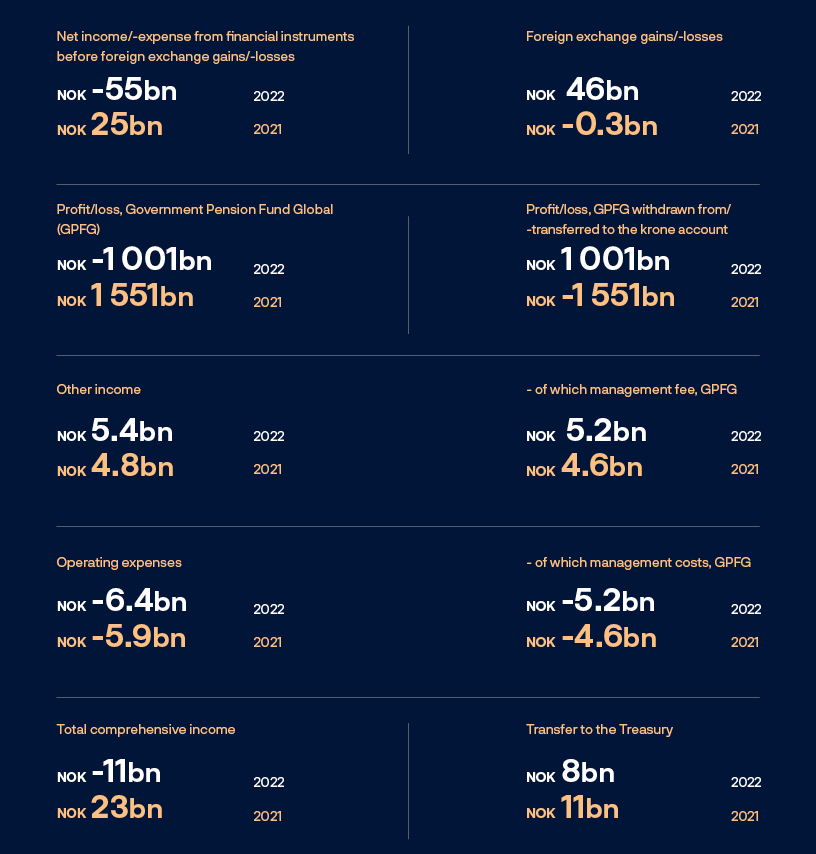

Net income/-expense from financial instruments

Net expense from financial instruments was NOK 55.1bn in 2022, compared with net income of NOK 24.2bn in 2021. Equity investments posted a loss of NOK 15.9bn, while fixed income investments posted a loss of NOK 38.3bn, compared with a gain of NOK 31bn and a loss of NOK 6.5bn, respectively, in 2021. Net income from financial instruments also includes a gain of NOK 45.5bn as a result of foreign currency effects. Foreign currency effects in 2021 resulted in a loss of NOK 0.3bn.

Government Pension Fund Global

The Government Pension Fund Global’s total comprehensive income showed a loss of NOK -1 001bn, comprising a loss on the portfolio of NOK -995.3bn and costs related to the management fee of NOK 5.2bn. Norges Bank’s total comprehensive income for 2021 amounted to NOK 1 551bn, comprising a gain on the portfolio of NOK 1 555bn net of management costs of NOK 4.6bn.

Total comprehensive income for 2022 was recognised against the GPFG’s krone account at 31 December 2022. The return on the portfolio, after management costs reimbursed to Norges Bank have been deducted, is transferred in its entirety to the krone account and thus does not affect Norges Bank’s total comprehensive income or equity.

Other operating income

In accordance with the management mandate for the Government Pension Fund Global, Norges Bank is reimbursed by the Ministry of Finance for its expenses related to the management of the fund up to a limit. Norges Bank was reimbursed in the amount of NOK 5.2bn in 2022, compared with NOK 4.6bn in 2021. Norges Bank also earns income from other services provided to banks and rent from external tenants. Income from these activities totalled NOK 149m in 2022, compared with NOK 118m in 2021.

Operating expenses

Operating expenses amounted to NOK 6.4bn in 2022, compared with NOK 5.9bn in 2021.

NOK 5.2bn of the operating expenses in 2022 is related to the management of the Government Pension Fund Global, compared with NOK 4.6bn in 2021. See Note 13 in the notes to the financial statements for more details on the management fee received by Norges Bank under the management mandate.

The increase in expenses compared with 2021 is mainly related to personnel expenses. Other than currency effects and ordinary wage growth, developments in personnel expenses primarily reflect a non-recurring effect in 2021 resulting from a change in the accrual accounting method for performance pay, the strengthening of the organisation in the form of more employees and increased travel. These developments are offset somewhat by, for example, lower fees to external managers of the Government Pension Fund Global.

Total comprehensive income

Change in actuarial gains and losses showed a loss of NOK 0.5bn in 2022, compared with a loss of NOK 0.1bn in 2021.

Norges Bank’s total comprehensive income for 2022 showed a loss of NOK 11.1bn, compared with a profit of NOK 23bn in 2021.

Distribution of total comprehensive income

The distribution of total comprehensive income follows guidelines on the reserves and on the allocation of Norges Bank’s profit, laid down by Royal Decree of 13 December 2019 pursuant to Section 3-11, Sub-section 2, of the Central Bank Act. Total comprehensive income shall be allocated to the Adjustment Fund until the Fund has reached 40% of the Bank’s net foreign exchange reserves. Any surplus is allocated to the Transfer Fund. A third of the Transfer Fund is transferred annually to the Treasury.

Norges Bank’s net loss of NOK -11.1bn will be covered by a transfer from the Adjustment Fund of NOK -13.2bn and a transfer to the Transfer Fund of NOK 2.1bn. NOK 8.1bn will be transferred from the Transfer Fund to the Treasury. The annual transfers and allocations for 2022 were made in accordance with the guidelines.

Norges Bank’s Executive Board

Oslo, 8 February 2023

Ida Wolden Bache (sign.)

Governor / Chair of the Executive Board

Pål Longva (sign.)

First Deputy Chair

Øystein Børsum (sign.)

Second Deputy Chair

Karen Helene Ulltveit-Moe (sign.)

Kristine Ryssdal (sign.)

Arne Hyttnes (sign.)

Hans Aasnæs (sign.)

Nina Udnes Tronstad (sign.)

Egil Herman Sjursen (sign.)

Mona Helen Sørensen (sign.)

Employee representative

Truls Oppedal (sign.)

Employee representative

An account of sustainability has been prepared pursuant to Section 3-3c of the Accounting Act. The report is presented in a separate document in the Annual Report. The report on sustainability is an integral part of the Executive Board’s report.

Norges Bank’s Monetary Policy and Financial Stability Committee

The Monetary Policy and Financial Stability Committee comprises the Governor, the two Deputy Governors and two external members.

The external members are appointed by the King in the Council of State for terms of four years. The Governor chairs the Committee, and the two Deputy Governors are first and second deputy chairs.

The Committee had 21 meetings and discussed 92 items of business within its area of responsibility in 2022.

The Committee’s work structure

The Monetary Policy and Financial Stability Committee is Norges Bank’s executive and advisory authority for monetary policy and also aims to contribute to promoting financial stability. The Monetary Policy and Financial Stability Committee normally holds eight scheduled meetings a year, where policy rate decisions are made. Four of the meetings coincide with the publication of the Monetary Policy Report (MPR). The level of the countercyclical capital buffer is also set by the Committee four times a year.1

The Committee’s meeting schedule is primarily determined by the dates of the eight monetary policy meetings. Prior to the meetings that coincide with the publication of the Monetary Policy Report, the Committee normally meets three times. Prior to the meetings without a report, the Committee normally meets twice.

In 2022, the Committee held 21 meetings and two one-day seminars. The Committee discussed the monetary policy strategy, the strategy for the countercyclical capital buffer, the Financial Stability Report and liquidity management, among other things.

The administration prepares and presents relevant analyses and projections that provide the basis for the Committee’s discussions and advises the Committee on policy decisions. To ensure that the discussion basis is as far as possible the same for all the Committee members, all are provided with as much access as possible to the same information and analyses.

The Committee is committed to transparent and clear external communication. The “Monetary policy assessment”, published in connection with policy rate decisions, and the “Assessment of the countercyclical capital buffer requirement”, published in connection with the buffer decisions, reflect the view of the majority. Topics of particular concern to the members in the discussions are highlighted in the assessment. Members that disagree with the assessment of the majority may dissent, and dissenting views are published together with a brief written explanation in the minutes and in the assessment published at the same time as the rate decision. All of the Committee’s decisions were unanimous in 2022. The Committee chair, the Governor, normally speaks on behalf of the Committee. Other Committee members may issue statements by agreement with the Committee chair.

1 From 2023, the decision will be made at the monetary policy meetings in January, May, August and November.

Members of the Monetary Policy and Financial Stability Committee

Ida Wolden Bache

Appointed Governor of Norges Bank from 8 April 2022 to 2028. Bache is Chair of the Executive Board and the Monetary Policy and Financial Stability Committee.

Pål Longva

Appointed Deputy Governor for the period 29 August 2022 to 2028. Pål Longva has particular responsibility for central banking operations and is First Deputy Chair of the Executive Board and the Monetary Policy and Financial Stability Committee.

Øystein Børsum

Appointed Deputy Governor for the period 2 August 2021 to 2027. Øystein Børsum has particular responsibility for the management of the Government Pension Fund Global and is Second Deputy Chair of the Executive Board and the Monetary Policy and Financial Stability Committee.

Jeanette Fjære-Lindkjenn

Appointed Committee member for the period to 31 December 2023.

Jeanette Fjære-Lindkjenn is a fellow at Housing LAB, the national centre for housing research at Oslo Metropolitan University (OsloMet). She has previously worked for DNB Markets as a macroeconomist and for Norges Bank as an analyst. Jeanette Fjære-Lindkjenn holds a degree in economics from the University of Oslo.

Ingvild Almås

Appointed committee member for the period to 31 December 2025.

Ingvild Almås holds a professorship at the Institute for International Economic Studies (IIES), Stockholm University, is Principal Investigator at the Norwegian School of Economics’ FAIR centre and International Research Fellow at the Institute for Fiscal Studies (London), Centre for Economic Policy Research (CEPR), and CESifo. She previously held a professorship at NHH. She sits on the Scientific Advisory Board for the Max Planck Institute for Research on Collective Goods in Bonn, Germany and chairs the Portfolio Board for Welfare, Culture and Society at the Research Council of Norway. In autumn 2023, Ingvild Almås will be a Cowles Foundation visiting fellow at Yale university. Ingvild Almås holds a BA in economics from the University of Oslo and a PhD in economics from the NHH Norwegian School of Economics.

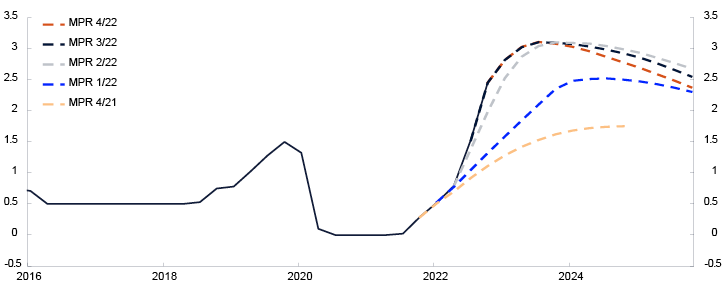

The year 2022 was marked by major shifts in the economic outlook. Owing to the post-pandemic recovery and Russia’s invasion of Ukraine, the world economy was beset by high inflation and uncertain growth prospects. When inflation in Norway accelerated in spring 2022, it became clear that the policy rate was no longer adapted to the prevailing economic situation. The policy rate was therefore raised more quickly and more markedly than the Committee envisaged at the beginning of the year.

In spring 2020, the policy rate was reduced to 0% to dampen the economic downturn caused by the Covid-19 pandemic. Economic activity rebounded in 2021, and Norges Bank started to raise the policy rate in September 2021. At year-end 2021, the policy rate was 0.5%. After the last pandemic-related restrictions were removed in 2022, activity picked up further and the labour market tightened. Inflation rose rapidly and eventually markedly overshot the 2% target. To ease the pressures in the economy and to bring inflation down towards the target, the policy rate was raised several times, to 2.75% at year-end 2022.

In autumn 2022, the Committee assessed that the outlook for financial stability was weaker than in 2021, reflecting the higher risk of an economic downturn in view of the ongoing war in Ukraine and the after-effects of the pandemic. The countercyclical capital buffer (CCyB) rate, which in March 2020 was reduced from 2.5% to 1.0%, was gradually raised again to 2.5% in the course of 2021 and 2022, with the rate fully effective from 31 March 2023. In November 2022, the Committee advised the Ministry of Finance to keep the systemic risk buffer (SyRB) for banks unchanged at 4.5%, and the Ministry followed the Committee’s advice.

Monetary policy

The global economy

The pandemic and related restrictions have caused large fluctuations in economic activity in recent years, both globally and in Norway. As most countries eased and later removed the restrictions, activity rebounded in the first half of 2021 and eventually exceeded pre-pandemic levels. The labour market improved, and wage growth began to rise.

At the same time, consumer price inflation rose markedly. In many countries, inflation reached levels not seen in decades. The rise in prices may partly reflect pandemic-related conditions. Lockdowns during the pandemic led to a shift in household consumption from services to goods. Strong demand for goods combined with production and transport bottlenecks led to rapidly rising prices for globally traded goods. Demand for commodities also picked up as the global economy recovered, and prices for energy, metals and agricultural products rose sharply.

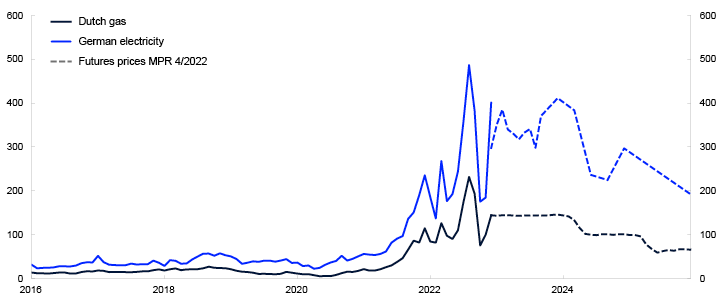

Russia’s invasion of Ukraine in winter 2022 led to substantial uncertainty about the global economic outlook and to a further increase in energy and other commodity prices. The decline in Russian gas supply to Europe pushed up gas and electricity prices to very high levels through summer. Gas and electricity prices edged down in autumn but remained high. In the latter half of 2022, prices for a number of other commodities fell. Oil prices, which had risen to around USD 110 per barrel in summer 2022, returned to close to USD 80 per barrel at year-end, broadly the same level as one year earlier. Global supply chain disruptions appeared to ease, and global freight rates fell substantially. Towards the end of 2022, consumer price inflation appeared to have passed its peak in some countries.

High inflation and prospects that inflation would also remain high ahead pushed up policy rate expectations among Norway’s trading partners through 2022. Central banks in many countries have raised policy rates to their highest levels in more than ten years. Several central banks have raised rates by larger increments than usual.

Economic activity among Norway’s trading partners rose further in 2022, and unemployment fell to low levels. At the same time, growth prospects weakened through the year, particularly in Europe. A number of firms scaled back production in response to high energy prices, and consumption growth was expected to slow on the back of high inflation and higher interest rates.

Uncertainty about energy market developments and the global growth and inflation outlook drove substantial movements in financial markets through 2022. Long-term interest rates rose substantially in 2022, while global equity indexes edged down.

Financial conditions in Norway

The krone exchange rate showed considerable volatility through 2022. Measured by the import-weighted exchange rate index (I-44), the krone depreciated somewhat through the year. Developments reflect a more pronounced rise in interest rates among trading partners than in Norway, as well as elevated financial market uncertainty.

Households’ interest payments have risen in pace with policy rate hikes. About 85% of the increase in the policy rate since autumn 2021 has passed through to mortgage rates. The pass-through from the policy rate to deposit rates has been weaker.

Corporate bank and bond financing has also become gradually more expensive. This is because both short-term and long-term interest rates have risen at the same time as bond market risk premiums have increased. There were large movements in the Norwegian equity market through 2022, but at year-end, the Oslo Børs Benchmark Index was broadly at the same level as one year earlier.

The Norwegian economy

Activity in the Norwegian economy picked up quickly in 2021, and in autumn that same year, capacity utilisation and employment returned to pre-pandemic levels. At the beginning of 2022, activity levels once again fell slightly owing to increased infection rates and pandemic-related restrictions. However, activity picked up quickly through spring. Growth was particularly strong in the sectors affected by the restrictions. Household consumption rose more than expected. Services consumption moved up quickly and eventually returned to pre-pandemic levels.

In pace with increasing activity levels, employment rose further, and unemployment fell faster than expected. Before summer, the enterprises in Norges Bank’s Regional Network reported growing shortages of intermediate goods and difficulties covering their labour needs. The Committee’s assessment was that activity in the Norwegian economy had reached a high level and that spare capacity was limited.

Through autumn, signs appeared that the economy was cooling down. High inflation curbed household purchasing power, and consumption growth slowed. Household confidence indicators were at very low levels. Nonetheless, economic activity held up better than expected, partly owing to higher private consumption but also owing to a substantial upward adjustment of business investment through the year. At the same time, Regional Network enterprises revised down their expectations for activity ahead, and in November, enterprises on the whole expected a significant decline in output over the next six months. The labour market remained tight, but labour shortages appeared to ease. Unemployment remained low, but the number of job vacancies declined.

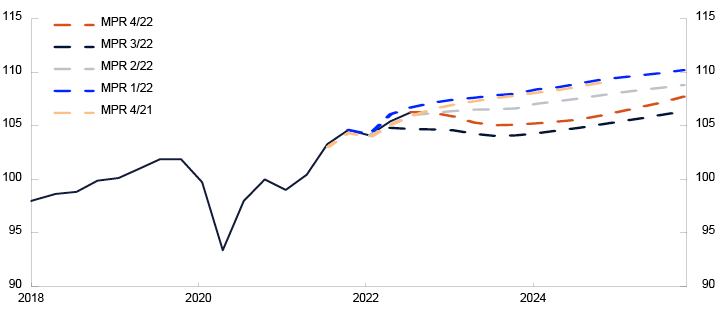

Chart 3 GDP for mainland Norway. Projections at different times. Index. 2019 Q4 = 100.

Sources: Statistics Norway and Norges Bank

Chart 4 Unemployment. Registered unemployment as a percentage of the labour force. 2016 Q1–2025 Q4.

Sources: Norwegian Labour and Welfare Administration (NAV) and Norges Bank

The housing market also reversed course during 2022. Strong demand and a small stock of unsold homes contributed to sustaining house price inflation through the first half of 2022, but the rise in prices slowed during summer. Through autumn, house prices fell. A large number of homes were listed for sale, and lower than normal turnover contributed to a marked upswing in the number of unsold existing homes in the market. In December, existing home prices were 1.5% higher than in the same month one year earlier.

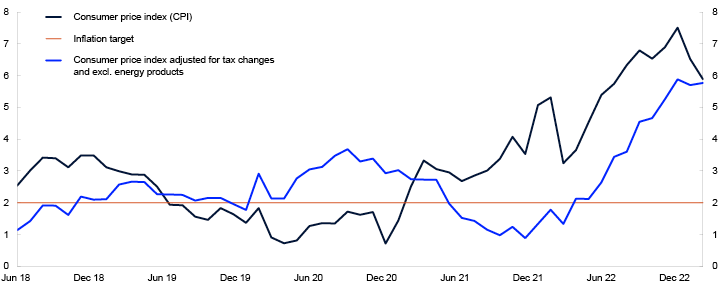

Consumer price inflation picked up faster than expected through spring and was markedly above the target. Owing to higher imported goods inflation and rising wage growth, inflation was expected to remain above target for some time. The rise in inflation continued through summer and autumn 2022. Energy and food prices showed a particularly steep increase through 2022, but prices for a range of other goods and services also increased more than normal.

Rising inflation likely helped to lift inflation expectations. Norges Bank’s Expectations Survey shows that inflation expectations for the coming years have risen since mid-2021. At year-end 2022, long-term inflation expectations were above the 2% inflation target.

The rise in the consumer price index (CPI) was restrained by government support for household electricity bills, a scheme introduced in December 2021. Even so, annual CPI inflation for 2022 was 5.8%, which is the highest annual CPI inflation rate since 1988. The consumer price index adjusted for tax changes and excluding energy products (CPI-ATE) rose by 3.9% in 2022, which is the highest annual rise since Statistics Norway began publishing the indicator in 2001. Prices for both imported goods and domestic goods and services rose at a rapid pace.

According to Statistics Norway, annual wage growth was 4.4% in 2022. Wage growth was higher than in 2021, reflecting a very tight labour market. There were prospects that wage growth would rise further in 2023.

Monetary policy trade-offs

The operational target of monetary policy is annual consumer price inflation of close to 2% over time. Inflation targeting shall be forward-looking and flexible so that it can contribute to high and stable output and employment and to counteracting the build-up of financial imbalances.

In its discussions of the monetary policy trade-offs through 2022, the Committee gave weight to the rapid rise in consumer prices and that inflation was turning out to be markedly above the target. The inflation forecasts were revised up, and there were prospects that inflation would remain high for some time. At the same time, economic activity had risen to a high level and unemployment was low. Through spring, it became clear that the policy rate no longer reflected prevailing economic conditions. The Committee gave weight to the need for higher interest rates to ease pressures in the economy and bring inflation down towards the target. The Committee also emphasised that a faster policy rate rise would reduce the risk of inflation becoming entrenched at a high level. The pace of policy rate hikes was faster, and the hikes steeper, than projected earlier.

Consumer price inflation remained high through autumn. At the same time, there were signs of a slowdown in the Norwegian economy, and the projections for capacity utilisation ahead were revised down. The Committee gave weight to the marked rise in the policy rate over a short period of time and that monetary policy was beginning to have a tightening effect on the economy. The policy rate was raised more gradually towards the end of the year.

Chart 5 Consumer prices. Twelve-month change. Percent.

Source: Statistics Norway

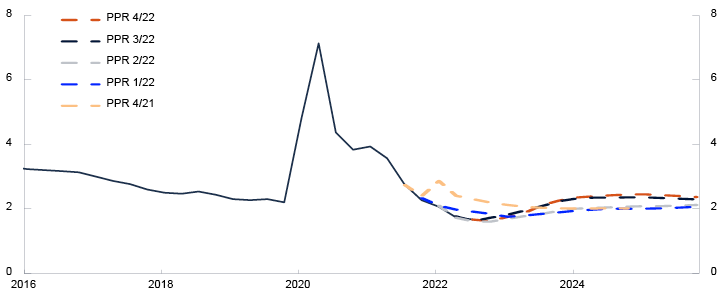

Chart 6 Estimated output gap. Percent. 2016 Q1–2025 Q4.

Source: Norges Bank

In its discussion of the balance of risks, the Committee’s concerns included the considerable uncertainty surrounding the outlook and that projections were more uncertain than normal. The Committee was concerned with balancing the risk of tightening too much against the risk of tightening too little. If the policy rate was raised too little, inflation could remain high for a longer period. If households and firms begin to become used to high inflation and adjust their price and wage setting behaviour accordingly, it may then become difficult to bring down inflation again. On the other hand, if the policy rate was raised too much, economic activity could contract more than what is necessary to bring down inflation.

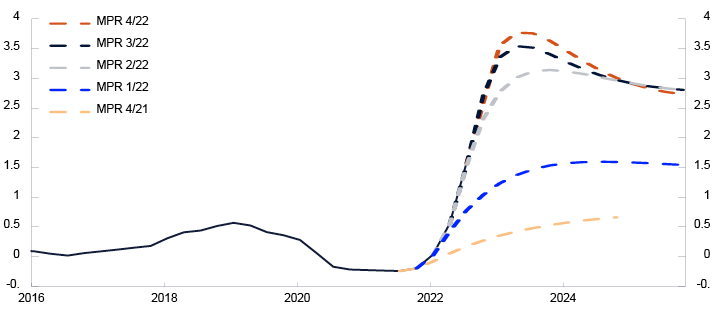

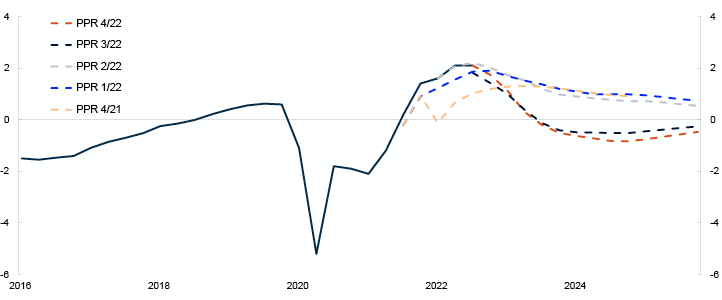

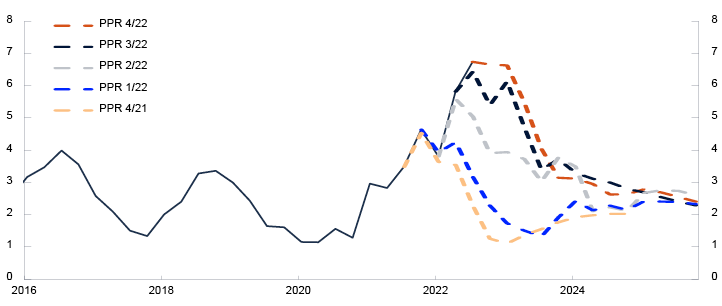

The projections in Monetary Policy Report 4/22 implied a policy rate of about 3% in 2023. Inflation was projected to drift down and approach the target somewhat further out. Capacity utilisation was expected to decline and remain slightly below a normal level in the coming years. Unemployment was projected to rise somewhat, albeit from a low level.

Chart 7 Consumer price index (CPI). Projections at different times. Four-quarter change. Percent.

Sources: Statistics Norway and Norges Bank

Monetary policy through 2022

The policy rate forecast at year-end 2021 implied a policy rate that gradually increased from 0.5% to about 1.75% over the coming years.

The policy rate path was revised up through 2022, particularly in the first half of the year. Owing to higher-than-projected capacity utilisation and an inflation forecast that was revised up, the policy rate was raised from 0.5% to 0.75% and the policy rate forecast was revised up at the monetary policy meeting in March. In the period leading up to the monetary policy meeting in June, inflation had been markedly higher than projected and unemployment had fallen more than expected. The policy rate was raised by 0.5 percentage point to 1.25%, and the policy rate path was revised up further.

Inflation continued to rise more than expected through summer, at the same time as unemployment fell to a very low level. The Committee raised the policy rate further to 1.75% at the monetary policy meeting in August and to 2.25% at the meeting in September. In September, the policy rate path was revised up somewhat, partly owing to prospects that inflation would remain high for longer. At the same time, there were signs of a slowdown in the Norwegian economy, and the projections for capacity utilisation were revised down considerably. At the meeting in November, the policy rate was raised by 0.25 percentage point to 2.5%.

In the period leading up to the December meeting, inflation had been higher than projected and the labour market slightly tighter. At the same time, it appeared that the slowdown in the economy would be somewhat more pronounced than previously projected. At the meeting in December, the policy rate was raised to 2.75%, while the policy rate path was little changed.

Financial stability