What should the future form of our money be?

Speech by Deputy Governor Jon Nicolaisen at the Norwegian Academy of Science and Letters, 25 April 2017.

Please note that the text below may differ slightly from the actual presentation.

Origins of the central bank

The Dutch financier Johan Palmstruch arrived in Stockholm in 1647. Some ten years later, he was granted permission to open a private bank, Stockholms Banco, where he combined two important innovations. The first of these, pioneered by Palmstruch, was to use customer deposits to fund lending. The second utilised Johannes Gutenberg’s invention, the printing press, to print the first European banknotes.

Stockholms Banco was authorised to issue banknotes backed by the copper and silver coins in use at the time. Coins could be deposited at the bank in return for banknotes, and banknotes could be exchanged for copper and silver at the bank. The banknotes proved to be popular and were soon in circulation.

Stockholm Banco also offered loans in the form of banknotes. For the Swedish king, Karl Gustav, this occurred at a convenient time. Wars were in progress that had to be financed, and a bank that would offer loans was like manna from heaven. King Karl Gustav made good use of the money. Sweden’s victory over Denmark-Norway in the 1658 Dano-Swedish War, leading to the permanent cession to Sweden of the strategically and historically important territory of Båhuslen in southeastern Norway, was thus at least partly the result of a financial innovation.

Things did not end well for Johan Palmstruch. There were no rules to limit the loans that could be issued by the bank, and Stockholms Banco’s loans far outstripped the value of the copper and silver held by the bank. Confidence in the banknotes began to evaporate, and their value fell. Demand to redeem the banknotes for copper and silver was high, but Stockholms Banco did not have enough metal to meet the demand, and Sweden experienced its first banking crisis. The bank was declared bankrupt and was liquidated. Johan Palmstruch was sentenced to death for irresponsible accounting. The death sentence was subsequently commuted, but Palmstruch had to spend the rest of his life in prison.

Nonetheless, the Stockholms Banco crisis left a permanent legacy: in 1668, the authority to conduct banking operations was transferred to a bank that was later to become the Riksbank, under the direct control of the Swedish parliament, Riksdagen.[1] The world’s first central bank was born.[2]

What is money?

So what is money exactly? The simple answer is that money is a means of payment. It is also a universally recognised common unit of account. Money has therefore a key role in all financial transactions – it is a practical means of assigning value to goods and services and of settling trades.

To perform these functions, money must have a fairly stable value. People will only accept money as payment if they believe it can be used again as a method of payment in the future. Money must therefore also function as a store of value.

The first coins to be struck, imprinted with the king’s mark as a guarantee of their weight, were produced in Lydia almost 2500 years ago – with the reverse bearing the mark of King Croesus. Since then, coins in a variety of metals have been widely used. The currency of Norway was directly linked to a metal for centuries, until the gold standard was abandoned in 1931.

Wealth in the form of silver and gold coins can – literally – be a heavy burden. The emergence of banknotes that could be exchanged for a specific monetary value in metal made it easier to manage large sums of money. A banknote is in reality a promissory note – an interest-free claim on the issuer. Its value depends on trust that the issuer will keep his word and that the banknote proves to have the promised value.

The issue of banknotes by private entities was a fundamentally unstable system. The solution was to establish central banks in order to build abiding trust in the currency. The Swedish central bank, the Riksbank, the first central bank in history, was founded because the issue of banknotes by a private bank – Stockholms Banco – led to a banking crisis. The origins of the US Federal Reserve are similar: during the so-called “free banking” era, private banks could issue their own banknotes in various denominations. However, the banks experienced repeated crises, and in 1913, the Federal Reserve was established to stabilise the private banking system.

In the post-war years, the value of western currencies was pegged to gold under the Bretton Woods system: an ounce of gold was worth USD 35. All the other member countries – including Norway – agreed to peg their currencies at a fixed rate to the US dollar. The gold standard was abandoned by President Nixon during the Vietnam War, and the traditional fixed exchange rate system was terminated in 1971.

The value of money is no longer linked to precious metals. Today, money is so-called fiat money. The term derives from the Latin “fiat”, meaning “let it become”.

In his book Sapiens – A Brief History of Humankind, Yuval Noah Harari writes: “Trust is the raw material from which all types of money are minted”.

And he goes on:

“..., the fact that another person believes in cowry shells, or dollars, or electronic data, is enough to strengthen our own belief in them, […]. Christians and Muslims who could not agree on religious beliefs could nevertheless agree on a monetary belief, because whereas religion asks us to believe in something, money asks us to believe that other people believe in something.”[3]

Money has value because – and only because – everyone believes in its value. Money is minted from trust.

But how is this possible? How can money retain stable value in a system exclusively based on belief and trust?

First, money must be usable. This is the domain of the authorities. All taxes in Norway must be paid in Norwegian kroner. The governments of most countries have defined the country’s banknotes and coins as legal tender. This means that a buyer is entitled to make a payment in the country’s currency, and a seller can require payment in this currency. Legal tender cannot be refused as payment by either party.[4] Buyer and seller can of course agree on a different method of payment if they so wish.

Second, trust is related to the role of the central bank. In most countries, it is taken as a matter of course that the central bank guarantees the value of the currency. The central bank is subject to democratic control. In Norway, Article 75 of the Constitution states that “It devolves upon the Storting [Norwegian parliament]… to supervise the monetary system of the realm”. At the same time, the people’s elected representatives have conferred independence on the central bank in the use of its instruments by means of the Norges Bank Act. This underpins trust in the central bank and ensures the democratic legitimacy of the system.

For Norway’s founding fathers, another important objective was to ensure that the king and his government did not have direct access to the banknote printing press. Past experience had shown that kings were not immune to temptation.

The stability of the value of the currency in Norway is guaranteed by Norges Bank, and ultimately by the Norwegian government. The authorities have delegated this task to Norges Bank and decided that the Bank’s monetary policy objective is to keep inflation low and stable. The inflation target is quantified in the regulation on monetary policy as annual consumer price inflation over time of close to 2.5 percent. The Bank’s policy instrument is the key policy rate. Confidence that inflation will be kept low and stable is underpinned by the central bank’s independence. Norges Bank has a clear mandate and an independent position. This fosters trust in the Bank’s ability to do its job.

But a regulation defining the inflation target and central bank independence are not enough. Confidence in the inflation target can only be upheld if the central bank actually ensures that inflation is low and stable over time, thereby maintaining monetary stability. Credibility and trust are built up over time. In Norway, inflation has been low and stable for a quarter of a century. As the expression goes, the proof of the pudding is in the eating.

How is money created?

Today, there are two forms of central bank money. One of the forms is common knowledge – banknotes and coins. The other, bank reserves at Norges Bank, is less well known. The sum total of banknotes and coins and bank reserves at Norges Bank is about NOK 85 billion.[5] But the total money supply is much larger than this. Customer deposits in banks are also money. These deposits, referred to as deposit money, total more than NOK 2 trillion in Norway. This money is created by banks, not by Norges Bank.

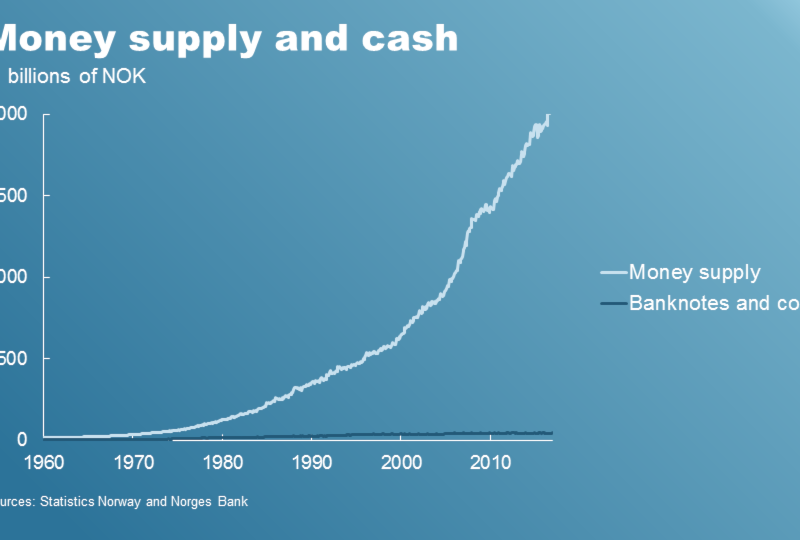

Chart 1: Money supply and cash

Chart 1 shows the money supply and the supply of banknotes and coins in Norway since 1960. In Norway, the money supply mainly comprises deposit money in banks.[6] In the early 1960s, banknotes and coins accounted for a fifth of the money supply. Current accounts and cheques were already becoming commonplace. Since then, banks’ deposit money has increased dramatically, and today, banknotes and coins make up less than 2.5 percent of the money supply. In other words, virtually all the money we use has been created by banks.

So how do banks create money? The answer to that question comes as quite a surprise to most people.

When you borrow from a bank, the bank credits your bank account. The deposit – the money – is created by the bank the moment it issues the loan. The bank does not transfer the money from someone else’s bank account or from a vault full of money. The money lent to you by the bank has been created by the bank itself – out of nothing: fiat – let it become.

The money created by the bank does not disappear when it leaves your account. If you use it to make a payment, it is just transferred to the recipient’s account. The money is only removed from circulation when someone uses their deposits to repay a bank, as when we make a loan repayment.[7] The money supply is therefore only reduced when banks’ claims on the rest of the economy decrease.

Banks also fund lending by raising loans themselves instead of creating money in the form of deposits. In order to reduce risk, banks also use other forms of investment in addition to lending.[8] Nevertheless, the money supply is growing at almost at the same pace as total bank credit.

To sum up: banks create money out of nothing and withdraw it when loans are repaid. Growth in total bank credit is normally matched by growth in the money supply.[9]

This does not sound encouraging. Is money an illusion? Why is today’s privately issued deposit money often perceived to be as safe as money issued by the central bank?

First and foremost, maintaining confidence that the deposits are safe is the responsibility of the banks. If a bank takes on too much risk, trust in that bank will be impaired. For trust to be maintained, it is essential that a bank operates responsibly.

Customer deposits in Norway are also covered by a deposit guarantee. For customers with accounts in Norwegian banks, the guarantee covers deposits of up to NOK 2 million per depositor per bank. This guarantee is provided by the Norwegian Banks’ Guarantee Fund, a joint deposit insurance scheme funded by Norwegian banks.

Nonetheless, probably the most important factor is that the banking sector is one of the most highly regulated sectors in society and is subject to strict supervision. A bank cannot operate without a licence, and banks are required to satisfy a number of requirements relating to capital adequacy and liquidity management, all of which limit bank lending and money creation. Norwegian banks cannot behave as Stockholms Banco did in the 1600s. By ensuring that banks are solid and sufficiently liquid, regulation and supervision also underpin trust in the money we use.

The financial crisis in autumn 2008 was triggered by the collapse of an under-regulated financial institution – the Lehman Brothers investment bank.[10] In the years preceding the crisis, Lehman’s equity was less than two percent of its assets. With so little capital supporting loans, it does not take more than a puff of wind to bring down a house of cards.

New forms of payment and new forms of money

Trust is necessary, though not sufficient, for money to function as a universal means of payment. It must also be efficient and safe to use.

When you make a payment in a shop using a bank card, one of the largest systems we have is set in motion. Payments move back and forth between banks. Banks settle the payments by transferring money between their accounts at Norges Bank. Your payment then becomes available in the recipient’s account, normally a few hours after the payment process was initiated.

The hub of the payment system in Norway is Norges Bank’s settlement system, and it is our responsibility to make sure the system is efficient and reliable. Turnover is substantial, and transactions totalling close to NOK 240 billion were settled by Norges Bank in 2016 – every day.

As a society, we are completely dependent on the smooth functioning of the payment system. Without a stable settlement system, it would not be possible to use customer deposits in bank accounts as a means of payment, and substantial resources are allocated, both by banks and by Norges Bank, to make the system as robust and efficient as possible.

Technological innovation continues to bring us new methods of payment. Using smartphone apps such as Vipps and MobilePay, we can now make payments using our mobile phones. Technology giants such as Apple, Samsung and Google are also entering the payment market. Suppliers of goods and services are making their own apps and linking them to bonus and loyalty programmes. Although this may be a positive trend for many people, it comes at a price. It is difficult for us as consumers to keep track of the information we disclose and how it is used. This poses a challenge to data privacy and the security of the payment system.

The apps are only a customer interface. Behind them lie international card schemes such as Visa and Mastercard. Even though users do not cover costs directly, the costs involved in using these schemes are high, making these solutions an expensive alternative for banks. Eventually, banks’ customers foot the bill one way or another.

Cheaper alternatives are on their way. The new solutions could also result in faster payments. National payment card schemes, such as BankAxept in Norway, might provide an alternative to the international card schemes, including access to the new services. New regulations have been introduced to lower the costs related to international cards. A new EU regulation also provides for direct bank-to-bank payments, bypassing the card schemes entirely.

Technological innovation has given us not only new methods of payment, but also new forms of money – so-called e-money. E-money is electronic money issued by non-bank entities, but in existing currencies. Paypal customers can make payments through their Paypal account. Facebook has recently applied for a Europe-wide e-money licence. If large providers offer an attractive, user-friendly solution, this method of payment could become widespread. A key issue related to e-money is the question of consumer trust. E-money is a claim on the issuing company. E-money is not backed by a deposit insurance scheme or any authority.

Other companies are offering new forms of money – often in the form of a new currency – on closed platforms such as social networks and online games. Examples of such platform currencies are Amazon Coins, the virtual currency used in the online game World of Warcraft and Chinese Q Coins. These currencies might seem insignificant, but they have already been used as means of payment outside their own platforms.

A number of private digital currencies have also appeared. Some have gained ground in terms of turnover and use, while others were introduced for purely fraudulent purposes and have rapidly disappeared. The largest and best-known digital currency is Bitcoin, which was launched in 2009. Bitcoin has been the subject of widespread debate, but still has only a minor role in the payment system. Payment by Bitcoin is costly, and the system’s capacity is limited. Bitcoin prices have been highly volatile. A characteristic of private currencies such as bitcoin is the absence of any central institution backing the currency. But this is also a problem, making it difficult to establish the trust necessary for a widespread adoption of these currencies.

Cybercrime

New technology and new forms of payment are raising fundamental questions related to the security of the payment system. Cybercrime is evolving rapidly, with cyberattacks becoming increasingly advanced and well-organised.

Central banks are also targeted. In February last year, an attempt was made to steal USD 950 million from the central bank of Bangladesh. Most of the payments were stopped, but in the course of 48 hours, USD 81 million had found its way to a bank in the Philippines. A few days later, more than USD 60 million had disappeared through Philippine casinos. As far as I know, the money trail stopped there.

All the institutions involved in our payment system are devoting increasing resources to prevent cyberattacks, from banks and Norges Bank to our security authorities. However, we can never be completely certain that the system will be able to resist all possible attacks. We can lose money too. Ultimately, there may come a time when our systems have to be shut down for a period.

We need to be prepared for a situation where the payment system – or parts of it – has to be shut down for a period. Contingency arrangements must provide protection against a wide range of incidents, not just cyberattacks. These arrangements primarily comprise a number of reserve solutions in our electronic systems. Our ultimate contingency and reserve solution is our banknotes and coins. This part of our contingency arrangements must be strengthened. On the advice of Norges Bank and Finanstilsynet (Financial Supervisory Authority of Norway), the Ministry of Finance recently circulated a consultation paper proposing a regulation to ensure the availability of cash in a contingency.

What should the future form of money be?

The role of banknotes and coins, which have been our central bank money since Norges Bank was founded a little more than 200 years ago, continues to diminish. Everyday payments are increasingly made using deposit money in bank accounts. New forms of payment are a new stage of this trend. This prompts the following question: what should the future form of money be?

There are perhaps some who believe that deposit money will ultimately become the sole means of payment. Because Norwegian banks are well-run and well-capitalised, and because customer deposits are covered by the deposit guarantee scheme, we trust deposit money. As long as this is the case, using deposit money will be cheap and efficient for the consumer. But is it entirely unproblematic?

Imagine an ordinary consumer, let’s call him Ola, in a future when cash is no longer in frequent use. Ola hasn’t been to a bank for many years. He hasn’t used cash for a long time. He pays for everything digitally. But now he’s worried. Over the past few weeks, there have been several major cyberattacks against the bank he uses. The bank’s systems have been down for hours at a time, and staff are working overtime to fix the problem.

Ola decides he wants his money.

He logs on to his online bank, which for the time being is still open. He considers his options: he could transfer his money to an account in another bank. Or he could transfer money to a pre-paid card. But Ola does not trust either option. Who is really behind these solutions? How safe are they now?

Ola decides he wants cash and contacts his bank. But the bank cannot meet his request as it is currently unable to provide Norwegian banknotes. Ola faces the same options as before: use an account in another bank? or a payment card? The only option that does not involve using another bank account is to buy bitcoins. Ola does not want to do this. Perhaps he is a little stubborn. He wants cash.

The bank clerk is patient. He tells Ola that the bank can offer dollar or euro banknotes. Ola sees no alternative and withdraws euro banknotes. But he soon encounters another problem. In order to use this currency to make purchases in Norway, the shop has to accept payment in euros. If not, Ola will have to deposit the euro banknotes in his bank account in order to make the payment – bringing him back to square one.

What has been lost here?

First, Ola has become completely dependent on a third party – the bank: payments can no longer be made directly between two parties, but must be channelled through a bank, a card company or an app. Today, you can settle a payment at a shop or with a neighbour in cash, without involving anyone else.

Second, Ola has become dependent on the technology functioning as it should. Technology is not needed to settle payments in cash – as long as cash is available.

Third, Ola is no longer anonymous when he makes a payment. All payment transactions using deposit money can be recorded. Anonymous payments are often associated with something negative, such as tax evasion or other criminal activity. But there is another side to anonymity – privacy. We may not be entirely comfortable with the thought that every purchase we make is recorded. It may be too reminiscent of the society described in George Orwell’s 70-year-old novel 1984.

Fourth, Ola no longer has access to money directly backed by Norwegian authorities. We no longer have functional legal tender. The monetary system has been turned over to private entities. Alternatively, Ola has to use another country’s currency – in our hypothetical case, the euro.

We have to ask ourselves: should we allow private solutions to compete freely in developing means of payment, or must the authorities play a role?

The crucial factor is whether solutions based on private money deliver the characteristics the payment system should have. The system must be able to channel payments swiftly, safely, at low cost and in a user-friendly manner. The means of payment itself – our money – must be universal, because money is only useful if it is widely used. This requires trust.

Deposit guarantee schemes and banking regulation promote trust. The objective of monetary policy is to maintain stability in the value of the currency. Norges Bank assists private operators in implementing faster and safer payments. We cooperate with other authorities to oversee and supervise the payment infrastructure to ensure robustness and efficiency. Privacy rules prevent unauthorised access to payment information.

But there are some characteristics deposit money lacks. It cannot offer anonymous payments. The system is vulnerable to advanced attacks. Having more money on deposit than is covered by the deposit guarantee scheme involves risk. Nor is direct and immediate settlement between two parties, without the involvement of a third party, possible without cash.

In the future, new payment solutions may be able to offer these possibilities. Private digital currencies providing anonymity are already on the market. These currencies can also be used even if banks’ systems fail – as long as the Internet is still functioning. The same applies to platform currencies and e-money. However, there are other crucial characteristics missing from these solutions – they are not backed by any authority and the level of foreign exchange and credit risk can be high.

One alternative currently being discussed is the introduction of electronic central bank money. There are several ways of achieving this: consumers can have an account either at the central bank itself or in a system controlled by the central bank. Another possible solution is for Norges Bank to issue a payment card or develop an app for consumers to use for anonymous payments.

Which brings us to another question: which means of payment should be the statutory form of legal tender in Norway if we introduce electronic central bank money? Should it be banknotes and coins, or Norges Bank’s electronic money, or both?

We must also ask ourselves what the consequences will be for the banking system. For many consumers, electronic central bank money could provide an alternative to deposit money in a bank, as cash does today. Banks can attract deposits through the interest rates they offer. But their ability to create money and extend credit could nonetheless be affected, especially if this new form of electronic money enters into widespread use.

Norges Bank has begun the work of assessing what the future form of money should be. This is a long-term process. Whatever the conclusion, we can be fairly certain that banknotes and coins will be with us for many years yet. Deposit money in banks will most likely continue to be the dominant means of payment, even if electronic central bank money is introduced. Nevertheless, the very fact that these questions are being raised heralds a new era for our monetary system.

Choosing the direction our future monetary system and payment system will take requires not only economists, but also technologists, lawyers and other social scientists. And political decisions will ultimately need to be made by our elected representatives. It devolves upon the Storting to supervise the monetary system of the realm.

The questions are numerous, but we already have one of the answers. Central banks were established to build confidence in the monetary system. That is still our primary task. We cannot leave the monetary system entirely in the hands of private entities. There will be a role for central bank money. We must have a legislative framework and a means of payment backed by the authorities to ensure trust in our money – as history has shown.

Thank you for your attention.

Footnotes:

- Riksbank website

- For more details about the story of Stockholms Banco and the origins of the Riksbank, see the Riksbank website

- Harari, Y.N. (2011) Sapiens: a brief history of humankind. Vintage Books, London, pp. 201 and 207.

- Definitions of legal tender vary across countries. Danish banknotes and coins, for example, are legal tender in Denmark, but this is a right for the payer and an obligation for the recipient of the payment, and not vice versa. See "Report on the Role of Cash in Society", The Danish Payment Council, August 2016: and Danmarks Nationalbank's Monetary Review, 3rd Quarter 2006, "Legal Tender".

- Bank reserves at Norges Bank are not included in the total money supply (M1, M2 and M3) as these reserves are financial institutions’ claims on other financial institutions. Claims between financial institutions or from the public sector are not included in the money supply.

- We refer here to the money supply measure M3, which includes time deposits, repurchase agreements, and bonds and short-term paper with a maturity of less than two years. We do not show M1, which only includes cash and customer deposits in banks, because there are substantial breaks in our historical series and M3 is comprised almost exclusively of deposits. In February 2017, repurchase agreements and bonds were 0.4 percent of M3. Time deposits represented a somewhat larger share at 9 percent of the money supply. For more details on money supply statistics, see https://ssb.no/en/bank-og-finansmarked/statistikker/pengemengde

For a review of Norway’s monetary history, see Eitrheim, Ø., J.T. Klovland and L.F. Øksendal (2017). A monetary history of Norway, 1816-2016, Cambridge University Press. - Deposit money is also reduced when customers withdraw cash. However, since cash is part of the money supply, the total money supply in the economy does not change.

- In isolation, diversification reduces banks’ funding risk. Increased use of wholesale funding may lead to slower growth in the money supply than in credit. Banks also hold liquidity portfolios containing highly liquid securities that can be sold to compensate for deposit withdrawals. This also reduces banks’ risk.

- For a more detailed explanation of how money is created by banks, see “Money creation in a modern economy”, Bank of England Quarterly Bulletin2014/Q1, and Bernhardsen, T., A. Kloster and O. Syrstad (2016) “Alternative virkemidler i pengepolitikken – Den nødvendige monetære økosirk” [Alternative monetary policy instruments – the necessary monetary circulation]. Staff Memo12/2016. Norges Bank (Norwegian only).

- Lehman Brothers was an investment bank and did not accept customer deposits. However, as the bank issued short-term paper and took part in repurchase agreements, which are included in M3, Lehman Brothers created money. The closure of Lehman Brothers led to investor flight from money market funds, very high money market volatility and higher demand for cash from US bank customers.